Is this cloud platform provider a buy?

- Luke Donay

- Sep 9, 2021

- 4 min read

It’s time to explore another cloud company. Here is the break down on $NET, otherwise known as Cloudflare.

Current Price: $127.99

52/Wk High: $132.09

52/Wk Low: $33.21

Market Cap: $40.0 Billion

3 Month Performance: 36.93%

Read below for the break down!

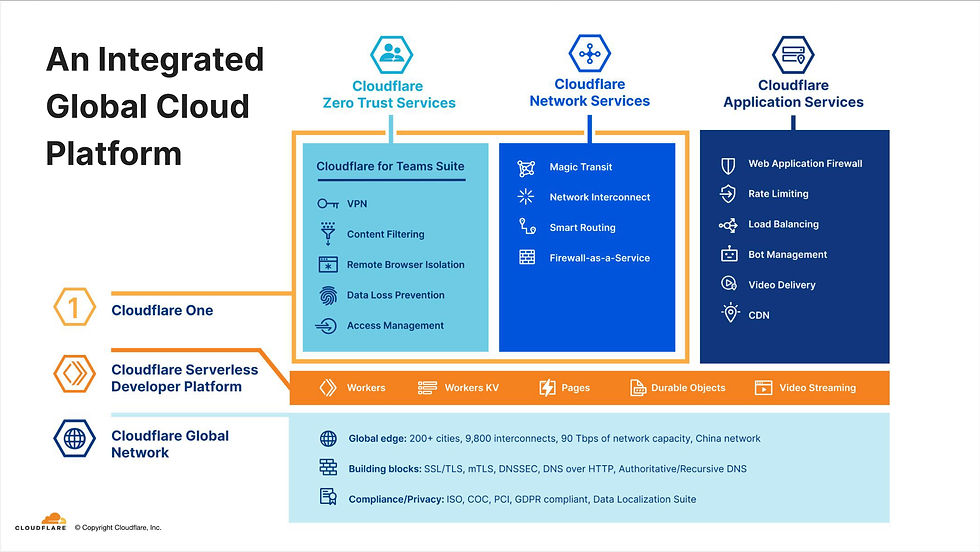

Cloudflare ( $NET ) is a major software and IT company that offers clients an advanced global cloud platform in which provides customers with a unified control plane boasting security, performance, and steadfast solutions through a bevy of cloud, on-premise, and SaaS applications.

Shifting into Cloudflare’s solutions the company’s products tend to serve various industries including eCommerce, SaaS, gaming, media, entertainment, public sector, and government industries.

Exploring Cloudflare’s customer base the company maintains a significant list of clients including HubSpot, Thomson Reuters, LendingTree, Shopify, Axios, SoFi, and over 126,000 paying customers as of Q2 2021.

The company is lead by Chief Executive Officer (CEO) and Chairman Matthew Prince, who took over leadership at Cloudflare in 2009. Prince boasts previous experience from the likes of Unspam Technologies, which he co-founded years ago.

In recent news, Cloudflare announced an upsized private offering of $1.125 billion in 0% convertible senior notes due 2026.

According to leadership, the offering will result in $1.1 billion in net proceeds that will go towards general corporate purposes, capital expenditures, potential acquisitions, “strategic” transactions, and working capital.

Digging into the numbers Cloudflare beat Q2 2021 expectations with an EPS of $-0.02, better than the analyst’s EPS consensus estimate of $-0.04. On a year-over-year basis, EPS improved by 33.33%.

Shifting into revenue, Cloudflare reported $152.4 million in Q2 2021 revenue, representing a strong 53% improvement year-over-year. Do note, Q2 2020 revenue totaled $99.721 million.

Alongside EPS and revenue, gross profit continued to expand on both a GAAP and non-GAAP basis. Cloudflare reported a Q2 2021 GAAP gross profit of $117.4 million and non-GAAP gross profit of $118.4 million, both of which are respectively higher than the Q2 2020 levels of $75.557 million and $76.586 million.

Coupled with gross profit, gross margins improved as well in Q2 with Cloudflare reporting a GAAP gross margin of 77% and non-GAAP gross margin of 78%, both of which are higher than their same time 2020 levels of 75.8% and 76.8%.

Touching on operating margins Cloudflare reported a GAAP operating margin of -18.9% and non-GAAP operating margin of -2.6% throughout Q2, both of which represent improvements over their Q2 2020 comparables of -24.8% and -9.5%.

While revenue, profit, and margins continued to improve Cloudflare reported an expanding operating loss and net loss. The company reported a Q2 2021 operating loss of $28.9 million, representing a larger operating loss than the same time 2020 operating loss of $24.7 million.

Furthermore, Cloudflare continued to run a net loss of $35.5 million, which when compared to the Q2 2020 net loss of $26.1 million, represents a significant expansion in net loss.

Rotating into cash flows Cloudflare reported an improved free cash flow (FCF) level of $-9.8 million, representing 6% of revenue. While FCF was negative, the Q2 2021 result represents an improvement over the same time 2020 FCF level of $-20.2 million.

Rounding out free cash flow metrics the company reported a Q2 2021 free cash flow margin of -6%, representing a sizable improvement over the Q2 2020 level of -20%.

Shifting into the customer front Cloudflare reported a whopping 126,735 paying customers at the end of Q2, representing 32% paying customer count growth year-over-year. The metric also marked the 8th straight quarter of customer count growth for the company.

Exploring the company’s customer base Cloudflare reported 1,088 customers producing over $100,000 in annualized revenue at the end of Q2, representing 71% expansion throughout the customer metric.

Finally, Cloudflare reported an improving dollar-based net retention rate of 124%, representing a sizable improvement over the same time 2020 level of 115% and small improvement over the Q1 2021 level of 123%.

Leadership was upbeat about the quarter.

“We had our strongest quarter ever as a public company, and our revenue growth continued to accelerate, growing 53%

year-over-year,” CEO Matthew Prince said.

Looking to the future leadership is bullish, expecting Q3 revenues to land within a range of $165 million to $166 million. The company also expects a Q3 non-GAAP loss from operations of $9.5 million to $8.5 million.

Guiding to the full year, management believes FY 2021 revenue will land within a range of $629 million to $633 million and that the company will run a non-GAAP loss from operations of $28 million to $24 million.

Shifting into the balance sheet the numbers are solid.

Total Debt: $401 Million

Total Liabilities: $645 Million

Total Assets: $1.446 Billion

Cash & Cash Equivalents: $247.551 Million

Analyzing the balance sheet Cloudflare experienced an increase in cash & cash equivalents as well as assets and liabilities on a year-over-year basis.

On a valuation basis, Cloudflare does trade at a premium.

Price to Sales: 74.42x

Price to Book: 49.30x

Management could be more effective going forward.

Return on Equity: -16.61%

Return on Assets: -9.68%

Return on Invested Capital: -10.93%

Given the numbers, the analysts are mostly neutral with a mean price target of $128.90/share, representing a minimal 0.71% upside.

The high price target is $140.00/share, representing a 9.38% gain, while the low price target is $105.00/share, representing a -17.96% downside.

The big money is quite involved with 82.86% of Cloudflare being owned by institutions. Top holders include Baillie Gifford & Co., Fidelity Management & Research, and Morgan Stanley Investment Management.

On a technical basis, Cloudflare has been on the move. According to the six-month charts, the MACD is moving with minimal upside momentum within a tight range around 3.26.

The six-month charts are also indicating an RSI of 60.51 and CCI of 112.33, both of which are on the high end.

Exploring investor sentiment the bears point to an extended valuation, sizable competitors, and increasing debt levels as indicators of downside.

Meanwhile, the bulls believe Cloudflare’s cutting-edge network and platform, reliable management team, and expanding TAM are indicators of future growth.

In short, Cloudflare ( $NET ) is a solid cloud company with over eight straight quarters of revenue, gross profit, and customer count growth coupled with a reliable management team, solid balance sheet, and expanding digital world.

EAT - SLEEP - PROFIT

Disclaimer: This is not direct financial advice, simply an opinion based on independent research.

Comments